The bedrock of the global financial system isn't gold or currency; it's the meticulous pooling of residential debt. You likely recognize that...

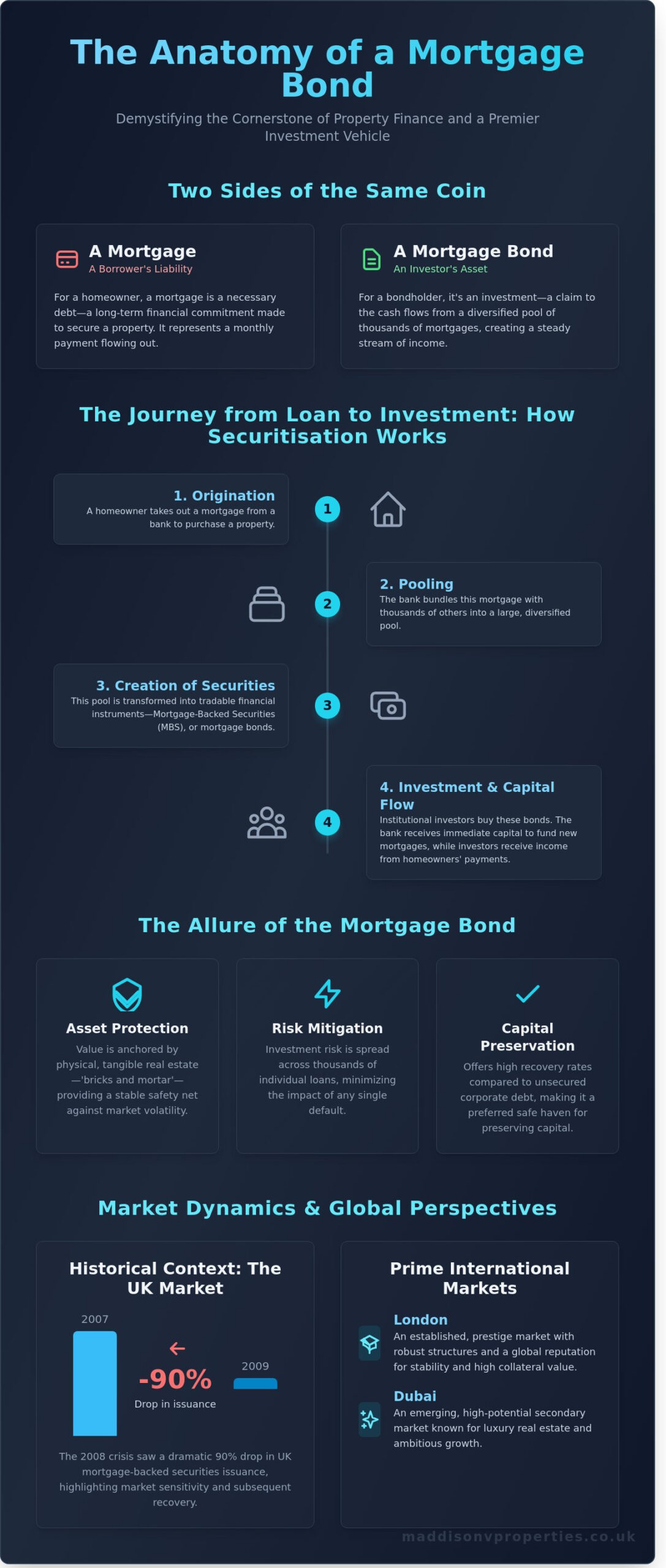

The bedrock of the global financial system isn’t gold or currency; it’s the meticulous pooling of residential debt. You likely recognize that property remains the ultimate asset class, yet asking what is a mortgage bond often leads to a labyrinth of jargon rather than clarity. Between the noise of US-centric financial news and memories of the 2008 liquidity crisis, when the UK mortgage-backed securities market saw a 90% drop in issuance between 2007 and 2009, it’s natural to feel a sense of hesitation.

Demystifying these secure financial instruments shouldn’t be a privilege reserved for institutional traders. This guide will clarify the complexities of property-backed securities to ensure you feel confident, informed, and empowered during your next portfolio review. We’ll explore how these bonds underpin the prime property market, drive essential liquidity, and dictate the rhythmic shifts in interest rates that define the luxury real estate landscape.

Key Takeaways

- Understand what is a mortgage bond and how these secured instruments function as a cornerstone of stability within a premium investment portfolio.

- Discover the meticulous process of securitisation and how it generates the vital liquidity necessary to fuel high-end property markets globally.

- Evaluate the risk-reward profile of property-backed securities to determine why they remain a preferred safe haven for preserving capital during market volatility.

- Navigate the nuances of international markets, from the established structures of London to the emerging, high-potential secondary markets in Dubai.

- Leverage professional insight into the bond market to transition from complex financial theory to securing a seamless, bespoke property acquisition.

Defining the Mortgage Bond: Security Beyond the Surface

Understanding what is a mortgage bond requires looking past the simple loan agreement to the sophisticated structure of institutional finance. At its core, a mortgage bond is a debt instrument secured by a meticulously selected pool of real estate mortgages. It’s a claim to the cash flow produced by a diversified pool of property loans. This structure offers a premium layer of security, as the bond’s value is anchored by physical, tangible assets rather than just a corporate promise. For the discerning investor, it represents a reliable, predictable, and structured way to access the property market’s rewards.

To better understand this concept, watch this helpful video:

The stability of these instruments often exceeds that of unsecured corporate debt. Because the underlying assets are residential or commercial properties, the investment carries an inherent, foundational value that remains even during market fluctuations. It’s this physical backing that transforms a standard financial product into a prestige asset class.

Mortgage Bond vs. Mortgage: Clearing the Confusion

It’s easy to confuse the two, yet they sit on opposite sides of the financial ledger. From a borrower’s perspective, a mortgage is a monthly commitment; it’s a necessary liability to secure a home. For the bondholder, it’s a bespoke investment opportunity. When asking what is a mortgage bond, you must see it as the mirror image of the debt. You aren’t just lending to one person; you’re receiving interest payments derived from thousands of borrowers. This transition from a single person’s liability to a diversified asset creates a seamless, high-quality stream of income for the investor.

The Role of Real Estate as Collateral

The true allure of a mortgage bond lies in its physical backing. If a default occurs, the process of asset liquidation begins to protect the bondholder’s interests. In prime markets like London and Dubai, the underlying value of real estate provides a reassuring, meticulous, and stable safety net. These cities maintain a global reputation for prestige and demand, ensuring that the collateral remains liquid and valuable. This physical nature adds a layer of peace of mind that unsecured investments simply cannot match. The bondholder benefits from a system designed for:

- Asset Protection: Secured claims on physical property.

- Risk Mitigation: Diversification across thousands of individual loans.

- Capital Preservation: High recovery rates compared to unsecured debt.

By anchoring wealth in the bricks and mortar of world-class cities, mortgage bonds offer a level of security that is both ambitious and grounded.

The Mechanics of Securitisation: How Bonds Fuel the Property Market

Understanding what is a mortgage bond requires a glimpse into the engine room of global finance. The process begins the moment a homeowner signs their mortgage deed. Rather than keeping that debt on their books for 25 or 30 years, banks bundle thousands of these individual loans together to create a single, tradable asset. This meticulous process, known as securitisation, transforms illiquid individual debts into property-backed securities that institutional investors can purchase with confidence.

This cycle is vital for the 2026 property market. When a bank sells these bundles, they receive an immediate influx of capital. This liquidity allows them to issue new loans to the next generation of buyers without waiting decades for monthly repayments. In the United States, “The Big Three” issuers-Fannie Mae, Freddie Mac, and Ginnie Mae-provide a government-backed foundation for this market. Private-label issuers, including major investment banks like Barclays or Goldman Sachs, offer additional bespoke options that cater to unique credit profiles. This constant flow of capital ensures the market remains fluid, sophisticated, and accessible.

Bundling and Tranches: Structuring the Investment

A mortgage bond isn’t a monolith. It’s a structured hierarchy of risk and reward. To attract a diverse range of investors, these bundles are divided into “tranches.” Senior tranches offer lower returns but carry the highest credit protection, while equity tranches provide higher yields for those willing to absorb the first losses. Most basic structures operate as pass-through securities, where interest and principal payments flow directly from homeowners to investors. More complex Collateralised Mortgage Obligations (CMOs) redirect these cash flows into specific schedules, offering a tailored experience for institutional portfolios. For those seeking a seamless property management solution, understanding these underlying structures reveals why the market remains so resilient.

The Impact on Interest Rates

The bond market acts as a barometer for the interest rates homeowners pay. There’s a direct, rhythmic relationship between bond demand and mortgage pricing. When global investors have a high appetite for these securities, lenders can offer more competitive rates to our clients. While the Bank of England base rate, which sat at 5.0% in August 2024, provides a benchmark, the “spread” or additional margin is determined by bond market efficiency. A healthy, transparent bond market reduces the cost of borrowing. It creates a stable environment where premium property investments can thrive, ensuring that the financial architecture supporting your assets remains robust and reliable through 2026 and beyond. This clarity is exactly what is a mortgage bond provides to the wider economy.

Evaluating the Investment: Risk, Reward, and Reliability

Investors frequently view property-backed debt as a sanctuary when traditional markets become turbulent. A mortgage bond serves as a defensive cornerstone, offering a level of predictability that equities cannot guarantee. This stability comes from the underlying physical collateral. Because these assets are secured by real estate, they carry less risk than unsecured corporate debt. This safety creates a classic trade-off; you accept lower yields in exchange for protected capital. It’s a choice for those who value peace of mind over speculative gains.

One specific nuance to monitor is prepayment risk. This occurs when borrowers pay off their mortgages ahead of schedule, often during periods of falling interest rates. While the return of principal is guaranteed, it can disrupt your long-term yield projections. Reinvesting that capital in a lower-rate environment may dilute your overall returns. In the hierarchy of fixed-income assets, mortgage bonds offer a unique intersection of physical security and predictable cash flow.

To truly grasp what is a mortgage bond, one must appreciate its role in a balanced portfolio. It acts as a rhythmic source of liquidity. It provides a steady pulse of income that remains independent of the stock market’s daily anxieties. For the investor seeking a premium, hands-off experience, understanding what is a mortgage bond is the first step toward a more resilient financial strategy.

Pros and Cons for the Sophisticated Investor

The benefits of these bonds include meticulous capital preservation and a bespoke income stream. They offer a seamless way to diversify without the volatility of direct property ownership. However, you must consider interest rate sensitivity. When the Bank of England raises rates, the market value of existing bonds can soften. Market liquidity also varies; some bonds are easier to trade than others. Success requires a steady approach backed by rigorous due diligence to ensure the underlying assets meet high standards. Investors who also hold direct property assets should consult a comprehensive buy-to-let mortgage guide to understand how rising rates and the April 2025 tax updates affect their broader financing strategy.

Lessons from History: 2008 vs. 2026

The memory of the 2008 subprime crisis often lingers, yet the regulatory framework in 2026 is vastly different. The Financial Conduct Authority (FCA) has implemented stringent oversight for property-backed securities in the UK, mandating higher transparency and stricter lending criteria. We’ve moved away from the systemic fragility of the past. Today, prime assets in prestigious locations like Chelsea or Marylebone are the benchmark for quality. These gold standard postcodes provide a layer of resilience, ensuring the investment remains as prestigious as the properties themselves.

Global Perspectives: Mortgage Bonds in London and Dubai Markets

Understanding what is a mortgage bond involves looking at how different regions secure debt against property. The UK market operates with a distinct level of precision compared to the highly institutionalized US system. While the US relies on massive government-sponsored entities like Fannie Mae, London’s landscape is shaped by private institutional lenders and a meticulous legal framework. This creates a stable, bespoke environment for those seeking premium returns through property-backed securities. When investors ask what is a mortgage bond in a global context, they’re often looking for the intersection of security, transparency, and long-term yield.

London’s Enduring Appeal for Institutional Lenders

The UK legal system provides a transparent foundation that protects bondholder rights with absolute clarity. Institutional investors favor London because its high-yield developments offer a level of security rarely found in volatile markets. Meticulous planning and a steady demand for corporate housing ensure these bonds remain attractive to global capital. For those looking to enter this space, consulting A Guide to Property Sourcing Agents in London provides the necessary local expertise to identify high-performance assets that underpin these financial instruments. International investors navigating the complexities of cross-border financing will find that a dedicated guide to securing a UK mortgage for international buyers is an essential resource for understanding deposit requirements, credit footprint challenges, and high-leverage financing strategies in 2026.

Financing Luxury in Dubai

Dubai’s financial landscape is evolving at an ambitious pace. By 2026, the city’s secondary mortgage market is expected to reach a new level of maturity, offering international investors unprecedented liquidity. The growth of off-plan financing is directly linked to a rising global appetite for Dubai-based debt. This momentum is sustained by the Golden Visa program, which saw a 52% increase in granted visas between 2022 and 2023. Understanding Why Invest in Dubai’s Property Market in 2026 is essential for anyone looking to capitalize on the strength of this emerging bond market. International buyers seeking to enter this market can find a comprehensive overview of financing options, including the current 50% Loan-to-Value limits, in this detailed guide to securing a dubai mortgage for non residents.

The MaddisonV Advantage lies in our ability to bridge these two world-class jurisdictions. We provide a seamless, hands-off, and meticulously managed experience for landlords who want to benefit from global property markets without the administrative burden. Whether you’re navigating the established streets of London or the ambitious skyline of Dubai, we ensure your investment is handled with prestige, reliability, and care. Before committing capital, sophisticated investors analyze a country’s bond market strength. It’s the ultimate indicator of liquidity, investor confidence, and long-term stability.

We handle the complex details of management so you can enjoy the rewards of a truly passive investment. Our approach is bespoke, seamless, and meticulous, ensuring your property remains a premium asset in any market cycle.

Navigating Financing with Meticulous Expertise

MaddisonV Properties operates at the intersection of financial intelligence and luxury real estate. Mastering the intricacies of the financial markets is the first step toward building a resilient property portfolio. When you understand what is a mortgage bond and how its yield influences lending rates, you gain a significant tactical advantage. We translate abstract market data into clear, actionable strategies for property acquisition. This ensures every decision is grounded in logic, stability, and market reality. Our team moves you seamlessly from the initial stage of understanding the bond market to the final moment of securing the property keys.

Bespoke Mortgage Consultations

Our team leverages a curated network of established lenders to identify competitive rates that reflect the current pulse of the bond market. This expertise ensures that whether you’re a domestic investor or an international buyer seeking entry into the UK market, your financing is structured with precision. We monitor shifts in the financial climate to help you secure terms that protect your long-term margins. Our approach is personal, sophisticated, and entirely focused on your unique financial goals. We remove the clutter of generic advice, providing a clear path to ownership through solutions that are bespoke, seamless, and meticulous. For landlords seeking to optimise their leverage in the current rate environment, our sophisticated investor’s buy-to-let mortgage guide outlines the precise strategies needed to navigate 5.2% interest rates and the latest tax-efficient financing structures.

Beyond the Bond: Full-Service Property Management

Securing the property is merely the beginning of the investment journey. A smart financing structure requires equally meticulous management to thrive as a high-performing asset. We offer a transition from acquisition to operation that ensures your investment remains entirely hands-off. By integrating premium facilities management with strategic financial planning, we eliminate the friction typically associated with landlord responsibilities. Our commitment to guaranteed rent provides the ultimate peace of mind. We handle the complex details of corporate housing, guest experiences, and maintenance so you don’t have to. The synergy between intelligent financing and professional management creates a truly passive, premium, and profitable income stream.

The financial landscape remains complex and ever-changing. Success requires more than just a basic grasp of what is a mortgage bond; it demands a partner who understands how these instruments dictate the rhythm of the property market. Professional advisory is a necessity for those who value their time and seek to build a legacy of high-quality assets. We provide the expertise needed to navigate this environment with quiet confidence and absolute clarity. Our goal is to handle the grit of management so you can enjoy the rewards of ownership.

Mastering the Future of Property-Backed Wealth

Understanding what is a mortgage bond allows you to navigate the complexities of securitisation with quiet confidence. These instruments provide a sophisticated bridge between liquid capital and the stability of the global property market. By leveraging the growth of the UK mortgage market, which the Bank of England valued at over £1.6 trillion in 2023, investors can secure reliable, asset-backed returns. In Dubai, the Land Department reported a 36.7% surge in transaction values last year, highlighting the immense potential of high-yield off-plan developments when managed with meticulous care.

Successful investing requires more than just capital; it demands a partner who understands the nuances of premium international markets. MaddisonV Properties provides the expertise needed to turn complex financial structures into seamless, high-quality outcomes. Our approach combines bespoke advisory for the London and Dubai sectors with comprehensive, hands-off management solutions. We handle every intricate detail so you can enjoy the rewards of a premium, luxury portfolio without the daily stress.

Secure your investment future with a bespoke mortgage consultation from MaddisonV Properties.

It’s a rewarding journey when you have the right expertise by your side.

Frequently Asked Questions

Is a mortgage bond the same as a mortgage-backed security (MBS)?

A mortgage bond is a specific type of debt security backed by a pool of home loans, while a mortgage-backed security (MBS) is the broader category for these financial assets. When you ask what is a mortgage bond, you’re looking at an investment that provides regular interest payments from the principal and interest paid by homeowners. In 2023, the global MBS market reached over $12 trillion, highlighting its scale as a cornerstone of modern finance.

Are mortgage bonds a safe investment for beginners in 2026?

Mortgage bonds offer a reliable, structured, and predictable income stream for beginners, provided they focus on investment-grade assets. By 2026, market forecasts from firms like Goldman Sachs suggest a stabilization in interest rates, making these bonds more attractive than volatile equities. Beginners should look for bonds with a Moody’s rating of Baa3 or higher to ensure their capital remains protected against market fluctuations. It’s a bespoke, secure, and prudent approach to wealth preservation.

How do mortgage bonds affect the interest rate on my home loan?

Mortgage bonds directly influence your home loan rates because lenders set their pricing based on the yields these bonds offer to investors. When investor demand for mortgage bonds increases, yields typically drop. This trend allowed 30-year fixed rates in the UK to average around 5.5 percent in early 2024. A robust bond market ensures a seamless, efficient, and competitive lending environment for every homeowner seeking premium financing options.

Can individual investors buy mortgage bonds directly?

Individual investors typically cannot purchase a single mortgage bond directly due to high minimum entry requirements, often exceeding £100,000. Instead, most people access this market through meticulous, diversified, and managed Exchange-Traded Funds (ETFs) or mutual funds. For instance, the iShares MBS ETF provides a liquid way to gain exposure to thousands of underlying mortgages without the complexity of direct ownership. It’s a professional, hands-off, and sophisticated investment strategy.

What is the biggest risk associated with mortgage bonds?

Prepayment risk is the most significant threat to mortgage bond investors, occurring when homeowners refinance their loans earlier than expected. This process forces investors to reinvest their capital at lower prevailing rates, often seen during the 2020 refinancing boom when rates dipped below 3 percent. Additionally, interest rate risk can devalue existing bonds if market rates rise, making the fixed payments from older bonds less competitive and less valuable.

Why do banks sell their mortgages as bonds instead of keeping them?

Banks sell mortgages as bonds to free up capital and maintain the liquidity necessary to issue new loans to the public. Under Basel III regulations, banks must hold specific capital reserves, so offloading these assets ensures they remain compliant and agile. This cycle creates a meticulous, rhythmic, and sustainable flow of credit, allowing financial institutions to serve more clients while transferring the long-term interest rate risk to secondary market investors.

How does the London property market influence bond values?

The London property market serves as a high-value anchor for UK mortgage bonds, as the city’s premium real estate often provides superior collateral. With London’s average house price reaching £508,000 in late 2023, bonds backed by these assets are often viewed as more secure. Strong performance in the capital boosts investor confidence, creating a prestigious, stable, and sought-after environment for bondholders who value the resilience of prime UK property.

What happens to a mortgage bond if the housing market crashes?

If the housing market crashes, the value of a mortgage bond typically declines as the risk of homeowner defaults increases. During the 2008 financial crisis, some subprime bond values fell by over 80 percent as foreclosures surged. However, bonds backed by high-quality, prime mortgages often retain their value better because they have larger equity buffers. Understanding what is a mortgage bond helps investors realize that asset quality is the ultimate protection against market volatility.

Sign Up Now

Want to read more great articles and blogs subscribe to our newsletter