– Hero Image")

In 2026, the era of the casual landlord is officially over. Success now belongs to the meticulous strategist who understands that navigating 5.2%...

In 2026, the era of the casual landlord is officially over. Success now belongs to the meticulous strategist who understands that navigating 5.2% interest rates and the April 2025 tax updates requires more than just capital; it requires a bespoke approach to leverage. You’ve likely realized that the UK property landscape has grown increasingly complex, where the margin for error has narrowed significantly since the 2024 regulatory shifts. This comprehensive buy-to-let mortgage guide is designed to restore your confidence, offering a clear path to securing tax-efficient financing while maintaining the premium standards your portfolio deserves.

We’ll show you how to master the intricacies of high-yield borrowing, navigate the EPC C requirements effectively, and unlock seamless financing options as an international investor. This article provides the clarity, the strategy, and the peace of mind you need to transition from a hands-on manager to a sophisticated owner of a fully managed, high-performance estate. By the end of this guide, you’ll have a meticulous roadmap for building a resilient, luxury portfolio that thrives in any economic climate.

Key Takeaways

- Navigate the intricate financial benchmarks of 2026, including Interest Cover Ratios and stress tests, to ensure your portfolio remains resilient and profitable.

- Utilize this comprehensive buy-to-let mortgage guide to master the nuances of interest-only structures and high-deposit requirements for maximum capital efficiency.

- Discover why a Limited Company (SPV) structure has become the preferred vehicle for tax-efficient growth and long-term wealth preservation.

- Anticipate the impact of EPC ‘C’ compliance and Stamp Duty surcharges to secure the most competitive lending rates in a shifting regulatory landscape.

- Transition toward a truly hands-off investment model by integrating bespoke property sourcing with meticulous, high-end management services.

Understanding the Buy-to-Let Mortgage Landscape in 2026

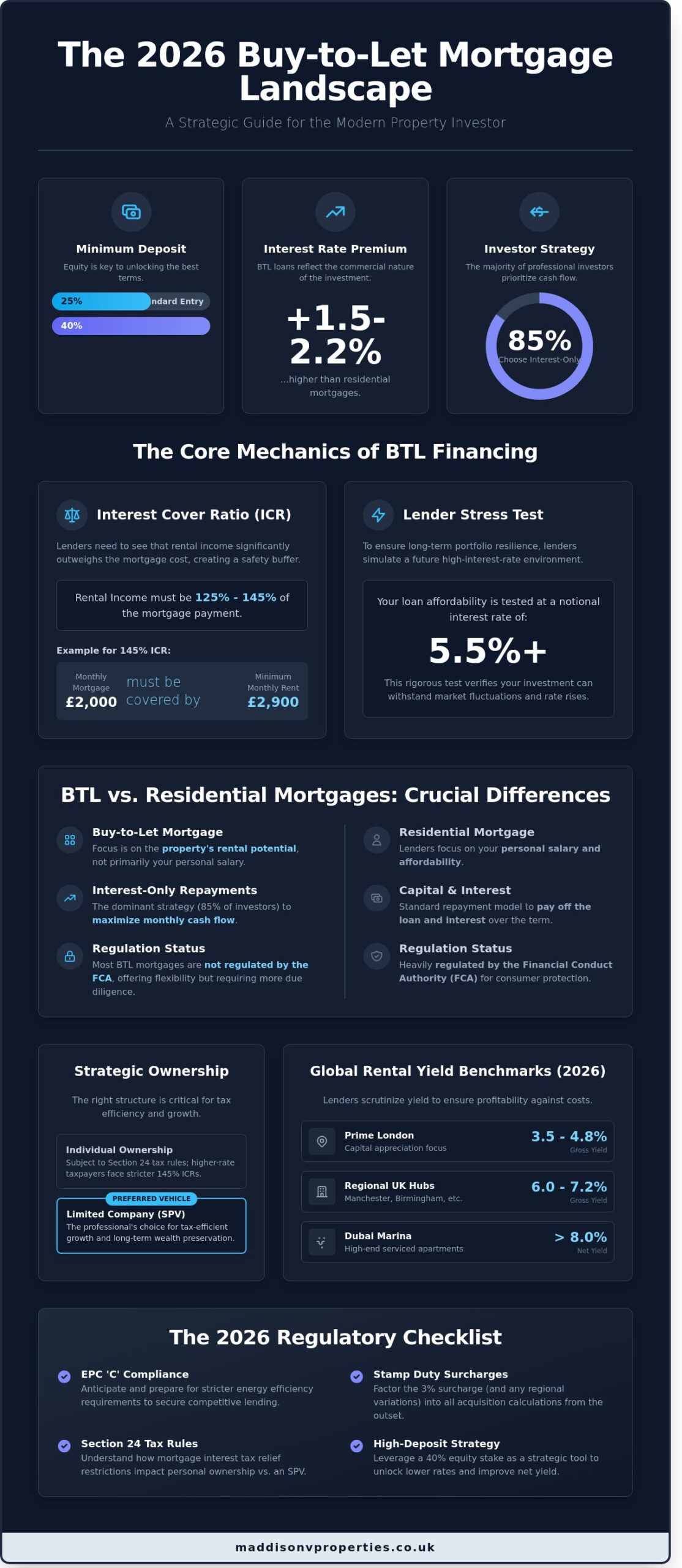

A buy-to-let mortgage is a bespoke financial instrument designed specifically for properties intended for rental purposes rather than owner-occupation. This buy-to-let mortgage guide highlights that these products differ fundamentally from residential loans in their structure, pricing, and risk assessment. As we move through 2026, the market has settled into a stable “new normal” following the rate volatility experienced between 2023 and 2025. Lenders now demand a minimum 25% deposit as a standard entry point, though the most competitive premium rates often require 40% equity to unlock the best terms.

Interest rates for these products typically sit 1.5% to 2.2% higher than standard residential loans. This premium reflects the commercial nature of the investment and the inherent risks of vacancy or tenant default. For investors targeting prime assets in London postcodes like W1 or high-growth districts in Dubai, professional mortgage advisory is intermediate. Navigating the cross-border tax implications and the meticulous lending criteria for high-value acquisitions requires a partner who understands the intersection of property and prestige. Furthermore, medical professionals with complex income structures may benefit from niche advisory services to ensure their status is correctly leveraged; read more about tailored mortgage advice for the medical community.

BTL vs. Residential Mortgages: The Crucial Differences

Lenders prioritize the property’s rental potential over your personal salary during the application process. While your income is a secondary safety net, the primary focus is the Interest Cover Ratio (ICR). Most lenders in 2026 require rental income to be at least 145% of the mortgage payment when tested at a stressed interest rate of 5.5%. Approximately 85% of professional investors choose interest-only repayments. This strategy maximizes monthly cash flow and provides a seamless way to reinvest capital into further acquisitions. It’s important to recognize that most BTL mortgages aren’t regulated by the Financial Conduct Authority, which offers greater flexibility but demands more rigorous due diligence from the landlord.

The Role of Rental Yield in Mortgage Approval

In the current 2026 lending climate, the “buffer zone” for rental coverage is more scrutinized than in previous years. Lenders look beyond the gross yield to ensure your investment can withstand maintenance costs and the 2026 tax environment. Gross yield provides a simple snapshot of performance, whereas net yield accounts for the meticulous details of management fees, insurance, and service charges.

Rental Yield is the annual rent divided by the property value, expressed as a percentage.

To secure approval in 2026, you should aim for these benchmarks:

- Prime London: Expect yields between 3.5% and 4.8%, where capital appreciation is the primary driver.

- Regional Hubs: Cities like Manchester or Birmingham often see yields of 6% to 7.2%.

- Dubai Marina: High-end serviced apartments frequently achieve net yields exceeding 8%, making the decision to invest in Dubai property a compelling proposition for yield-focused portfolio diversification.

Securing a buy-to-let mortgage guide that balances these yields with your long-term wealth goals ensures a hands-off, sophisticated investment experience. This rhythmic approach to portfolio building provides the peace of mind that your assets are performing at their peak potential.

The Mechanics of Financing: ICR, Stress Tests, and Deposits

Securing capital in 2026 requires more than a healthy credit score; it demands a meticulous understanding of how lenders quantify risk. The Interest Cover Ratio (ICR) remains the primary metric for any comprehensive buy-to-let mortgage guide. Most lenders require rental income to reach 125% to 145% of the mortgage payment. If your monthly interest payment is £2,000, your property must generate £2,900 in rent to satisfy the 145% threshold. This buffer protects against maintenance costs, unexpected repairs, and void periods, ensuring your investment remains a stable asset rather than a liability.

Stress testing has become significantly more rigorous over the last 24 months. Lenders now simulate interest rates of 5.5% or higher to verify your portfolio’s long-term resilience. While a 25% deposit is the standard minimum, sophisticated investors often target a 40% equity stake. This specific threshold typically unlocks premium product tiers. These tiers can reduce interest rates by as much as 0.85% compared to high-LTV options, which significantly improves your net yield and monthly cash flow. It’s a strategy that prioritizes quality over quantity. Understanding how lenders pool and securitize residential debt through what is a mortgage bond and how property-backed securities work can further illuminate why these stress test thresholds are set at their current levels.

Calculating Your Borrowing Power

Your personal tax bracket directly impacts your borrowing capacity due to Section 24 regulations. Higher-rate taxpayers usually face the stricter 145% ICR requirement because mortgage interest isn’t fully deductible. You can improve your standing by presenting a professional management plan. Lenders view properties managed by specialists as lower risk; this often justifies higher rental projections during the application process. Clear, declarative financial data is your strongest tool when negotiating these terms.

Specialist Lenders vs. High Street Banks

High street banks prioritize volume and simplicity. They frequently reject complex luxury developments, off-plan builds, or properties with unique architectural features. Boutique lenders and private banks offer a bespoke advantage. They provide flexible underwriting, higher LTV options, and the rapid execution required for prime London acquisitions. MaddisonV maintains an exclusive network to help secure financing for prestige developments in Marylebone and Chelsea. If you seek a seamless and hands-off experience, aligning with a partner who understands the nuances of luxury property is vital. Our approach ensures your portfolio is managed with the same meticulous care you put into your financing strategy.

- ICR Benchmarks: Aim for 145% to ensure maximum lender flexibility.

- Stress Tests: Prepare for simulations at 5.5% to 6% interest rates.

- Deposit Targets: Use 40% equity to access the most competitive, premium rates.

- Bespoke Lending: Use private banks for non-standard or luxury assets.

Strategic Ownership: Individual vs. Limited Company SPV

The architecture of property ownership has evolved into a meticulous exercise in tax efficiency and long term wealth preservation. By 2026, data from the UK’s Companies House suggests that over 82% of new buy-to-let mortgage guide applications originate from Special Purpose Vehicles (SPVs) rather than individual names. This shift reflects a strategic response to a tax regime where personal ownership often subjects rental income to rates as high as 45%. In contrast, corporation tax remains a more manageable 25% for profits exceeding £250,000, providing a stable foundation for portfolio growth. The market for limited company mortgages has matured significantly; lenders now offer competitive, bespoke products that mirror the rates once reserved for individual borrowers.

The Benefits of the Special Purpose Vehicle (SPV)

Operating through an SPV offers a level of financial agility that personal ownership cannot match. It provides a seamless way to manage assets while securing your legacy through a structure designed for longevity. Professional investors choose this route for three primary reasons:

- Full interest deductibility: SPVs allow you to deduct 100% of mortgage interest from rental income before tax is calculated, bypassing the restrictive Section 24 rules that impact individual higher rate taxpayers.

- Portfolio scaling: Retained profits within a company structure are only taxed at the corporate rate, which makes it easier to reinvest capital into new premium acquisitions without the sting of personal income tax.

- Succession planning: Transferring shares in a limited company is often more efficient than transferring physical titles, reducing the complexities and friction associated with inheritance tax.

Financing for the Global Investor

For the sophisticated investor managing assets between London and Dubai, the mortgage market has become increasingly integrated. Lenders now provide premium, hassle-free products tailored for non-residents and UK expats who demand speed and reliability. In Dubai, the landscape remains robust with Loan-to-Value (LTV) limits typically capped at 75% for residents and 60% for non-residents, often supported by meticulous developer backed financing. Mortgages for non-resident investors generally require a deposit between 35% and 50% depending on the specific jurisdiction and lender criteria. Those looking to invest in Dubai property with a data-driven, tax-efficient strategy will find that understanding these LTV thresholds is essential to structuring a resilient cross-border portfolio. This capital requirement ensures a stable, low risk environment that protects the integrity of your global portfolio. It’s a structure that offers peace of mind, allowing you to focus on the lifestyle benefits of your investments while the technical details remain handled. Overseas investors navigating these cross-border complexities will also benefit from understanding how to secure a uk mortgage for international buyers, where specialist lenders offer bespoke products designed to overcome the unique challenges of a missing UK credit footprint.

Choosing the right vehicle is about more than just the immediate buy-to-let mortgage guide rates; it’s about building a premium, scalable future. Whether you’re looking at a luxury apartment in Mayfair or a high floor residence in Downtown Dubai, the ownership structure you choose today dictates your financial freedom tomorrow. For those looking to further secure their family’s global standing, it may also be beneficial to explore Cidadania Portuguesa para Filhos as part of a multi-generational wealth and mobility plan.

The 2026 Regulatory Checklist for Buy-to-Let Landlords

The regulatory landscape of 2026 demands a meticulous approach to compliance. Investors can’t afford to view energy efficiency as a secondary concern. An EPC rating of ‘C’ is now a fundamental requirement for accessing the most competitive products found in any buy-to-let mortgage guide. Lenders prioritize sustainability, often rewarding high-end new builds with lower interest rates through bespoke Green Mortgage products. These incentives can reduce interest rates by up to 0.25% for properties that exceed the minimum environmental standards, directly improving your net yield.

Stamp Duty Land Tax remains a primary consideration for portfolio expansion. The 3% surcharge for additional properties is a fixed reality of the 2026 market, necessitating precise capital planning from the outset. In prime London boroughs, mandatory licensing has expanded significantly. Selective and HMO licensing requirements in areas like Camden, Westminster, and Southwark are rigorous. They focus on maintaining the prestige of the local rental market and ensuring superior guest experiences. Securing these licenses early ensures your investment remains a hands-off, premium asset rather than a legal burden. Failure to comply with these local standards can result in civil penalties of up to £30,000.

Preparing Your Application for Success

Securing a mortgage in 2026 requires a structured three-step process to ensure a seamless approval. Start by gathering three years of tax returns and verified proof of rental income from your current holdings to demonstrate stability. Next, verify that your target property hits the mandatory EPC ‘C’ benchmark to qualify for the best market rates. Finally, secure an Agreement in Principle before you enter negotiations for off-plan units. This builds confidence with developers and positions you as a serious, ready-to-act investor in a competitive market. Understanding the full mechanics of off-plan property investment is essential at this stage, as the unique financing timelines and exchange deposit structures require a distinct approach compared to standard completed properties.

Navigating the 2026 Tax Environment

The current tax environment emphasizes the need for professional oversight. Capital Gains Tax (CGT) rates for residential property disposals remain a critical factor when you’re considering a sale or portfolio reshuffle. Meticulous bookkeeping is the only way to ensure your tax reporting is accurate and optimized for all available reliefs. It’s helpful to review a Due Diligence Checklist for UK Property Investors to align your strategy with these latest fiscal requirements. Professional property management helps bridge the gap between complex tax obligations and the rewards of ownership.

The MaddisonV Approach: Seamless Sourcing and Financing

A sophisticated investment strategy requires more than just a competitive interest rate. While this buy-to-let mortgage guide has detailed the technical landscape of 2026, true wealth preservation stems from an integrated approach that connects sourcing, financing, and meticulous management. At MaddisonV, we believe the most successful investors aren’t those who manage every detail themselves, but those who partner with experts to ensure a truly hands-off experience. Our bespoke advisory service focuses on securing high-performance assets in global hubs like Chelsea, Marylebone, and Dubai, where we currently target gross yields of 7.2% for our private clients.

Securing the right deal requires a bridge between market data and execution. Our mortgage consultations serve this purpose, ensuring your financing structure aligns with the physical asset’s potential. We manage the complex, gritty details of property acquisition so you can focus on the rewards of ownership. This commitment to a seamless journey is why we prioritize facilities management as a core pillar of our service. By maintaining properties to an aspirational, luxury standard, we protect your capital and ensure the consistent yields you expect from a premium portfolio. Discover how our bespoke property management strategy for sophisticated investors in 2026 transforms demanding assets into seamless, high-performing investments.

From Sourcing to Success-Based Fees

We identify off-market opportunities that high-street investors never see, utilizing a network where 64% of our 2025 transactions occurred before reaching public portals. Working with dedicated property sourcing agents London investors trust ensures you gain first access to the capital’s most sought-after acquisitions before they ever reach a public listing. There’s a powerful synergy between property sourcing and mortgage arrangement; having a pre-approved, strategic finance plan allows us to move with the speed required in competitive markets like London and Dubai. A significant proportion of these exclusive opportunities involve off-plan property investment in prime locations like Chelsea and Dubai, where securing assets years before completion delivers the most substantial capital growth for our private clients. Our model is built on transparency and alignment with your goals. For a detailed breakdown of how we partner with you, please review Our Property Sourcing Fee Structure Explained. We ensure our success is directly tied to the value we create for your portfolio.

Your Next Step: A Free Mortgage Consultation

Your journey toward a refined, hands-off portfolio begins with a bespoke mortgage consultation. During this session, we’ll perform a comprehensive portfolio review, conduct a granular rate comparison, and develop a strategic plan tailored to your long-term objectives. We’ll help you position your assets to capture the 4.8% capital growth projected for prime London locations throughout 2026 while maximizing immediate rental income through our serviced accommodation model. It’s time to move beyond the standard buy-to-let mortgage guide and into a partnership that values your time as much as your capital. We provide the reliability, prestige, and expertise you need to scale with confidence.

Future-Proofing Your 2026 Investment Strategy

Navigating the current market requires a shift from passive ownership to strategic precision. This buy-to-let mortgage guide underscores that mastering 2026 ICR requirements and utilizing Limited Company SPVs are no longer optional for the serious investor. Successful landlords are currently adapting to the 145% interest cover ratio benchmarks while focusing on high-growth prime markets. It’s about ensuring every asset is structured for maximum stability, tax efficiency, and long-term appreciation.

MaddisonV offers a sophisticated, all-encompassing solution for those seeking a truly hands-off experience. We provide exclusive access to off-plan luxury developments in Chelsea, Marylebone, and Dubai; this ensures your capital is placed in the world’s most resilient locations. Our team manages the meticulous details of property and facilities management, allowing you to enjoy the rewards of a premium portfolio without the daily complexities. We pride ourselves on delivering a service that is bespoke, seamless, and reliable.

The right partnership transforms a complex financial endeavor into a streamlined path toward wealth. We look forward to helping you build a legacy of exceptional property assets.

Secure your bespoke property investment with MaddisonV

Frequently Asked Questions

How much deposit do I need for a buy-to-let mortgage in 2026?

You typically need a minimum deposit of 25% for most investment properties in 2026, though premium lenders often require 35% or 40% for larger loan-to-value security. This initial capital ensures you access more competitive rates and protects your equity against market fluctuations. For a £500,000 investment, expect to provide at least £125,000 upfront to secure a bespoke financing package that aligns with your long-term wealth strategy.

Can I get a buy-to-let mortgage if I am a first-time buyer?

You can obtain a buy-to-let mortgage as a first-time buyer, although your choice of lenders is restricted to roughly 20% of the major UK providers. Lenders apply meticulous criteria, often requiring a minimum personal income of £25,000 and a larger deposit of 25% or more. This buy-to-let mortgage guide highlights that while it’s possible, securing professional advice is essential to navigate these more complex underwriting requirements successfully.

Is it better to buy property in my own name or through a limited company?

Investing through a limited company is often more tax-efficient because you can deduct 100% of mortgage interest from your rental income before paying corporation tax at the current 25% rate. If you buy in your own name, you only receive a 20% tax credit, which significantly impacts higher-rate taxpayers in the 40% or 45% brackets. Most sophisticated investors now choose the corporate structure to ensure a seamless and scalable property portfolio.

What is a ‘Stress Test’ and how does it affect my borrowing?

A stress test is a calculation lenders use to ensure your rental income covers the mortgage payments, typically requiring a 145% coverage ratio at a hypothetical interest rate of 6.5%. This ensures your investment remains viable even if market conditions shift or rates rise unexpectedly. By meeting these rigorous standards, you gain the peace of mind that your cash flow can withstand various economic cycles without ever compromising your financial stability.

Can international buyers or non-residents get a mortgage in the UK?

International buyers and non-residents can certainly secure UK financing, though they typically face a higher deposit requirement of 35% to 40%. Specialist lenders provide bespoke products tailored for overseas investors, focusing on the quality of the asset and your global financial standing. For a comprehensive breakdown of the specific criteria, deposit thresholds, and lender options available to overseas investors, our dedicated guide to UK mortgage for international buyers in 2026 provides the strategic roadmap you need. This approach allows global clients to enjoy the prestige of UK property ownership while benefiting from a professional, hands-off management experience that protects their international capital.

How do EPC ratings affect my ability to get a buy-to-let mortgage?

Properties with an EPC rating of C or higher now qualify for “green” mortgage products that offer interest rate discounts of approximately 0.2% to 0.5%. Lenders are increasingly cautious about assets rated D or below, as upcoming 2028 regulations mandate higher energy efficiency standards for all rental properties. Ensuring your portfolio meets these meticulous environmental standards is a vital part of any modern buy-to-let mortgage guide to maintain long-term asset value.

What are the current interest rates for buy-to-let mortgages in London?

Current interest rates for London buy-to-let mortgages in early 2026 range from 4.2% for a 60% loan-to-value product to 5.8% for higher-leverage options. These figures reflect the premium nature of the capital’s real estate market and the stability of its rental demand. Securing a fixed rate for five years provides the predictable, hassle-free financial foundation that sophisticated investors require to manage their high-end London portfolios with absolute confidence.

Can I use a buy-to-let mortgage for a short-term or serviced accommodation property?

You must use a specialist serviced accommodation mortgage rather than a standard buy-to-let product if you intend to offer short-term stays. These bespoke loans account for the higher yields of corporate housing, often requiring a 150% interest cover ratio to mitigate the increased operational complexity. This financing structure allows you to leverage the high-quality guest experiences we provide while ensuring your lending remains fully compliant with meticulous institutional requirements.

Sign Up Now

Want to read more great articles and blogs subscribe to our newsletter