What if the traditional route of personal property ownership isn't just inefficient, but a direct threat to your long-term wealth? In 2026, the...

What if the traditional route of personal property ownership isn’t just inefficient, but a direct threat to your long-term wealth? In 2026, the strategic landscape of financing a property portfolio within a limited company has evolved from a niche tax maneuver into the essential foundation for any serious London investor. With 66,587 new buy-to-let companies registered last year alone, the shift toward incorporation is no longer a trend; it’s a standard for those seeking to protect their margins against the persistent weight of Section 24.

It’s natural to feel a sense of hesitation when faced with the administrative complexity of a Special Purpose Vehicle or the anxiety of fluctuating interest rates. You’ve worked hard to build your capital, and you deserve a structure that offers both financial security and mental tranquility. This article promises to help you master the sophisticated financial frameworks required to scale a high-yield portfolio in prestigious districts like Canary Wharf or Nine Elms while maintaining effortless oversight.

We’ll provide a clear roadmap through the 2026 tax landscape, covering everything from the 25% Corporation Tax main rate to the nuances of the £500 dividend allowance. You’ll discover how to transform a collection of assets into a professionally managed, tax-efficient legacy that provides stable returns and long-term peace of mind.

Key Takeaways

- Understand why the 2026 tax landscape makes incorporation the primary choice for professional landlords seeking to bypass Section 24 restrictions.

- Learn the precise mathematical advantages of financing a property portfolio within a limited company to maximize your post-tax rental yields and reinvestment potential.

- Discover why high-growth districts like Nine Elms and Canary Wharf offer the most resilient opportunities for corporate-structured new build investments.

- Identify the break-even point where corporate borrowing costs are outweighed by the benefits of full mortgage interest deductibility.

- Gain insights into how professional management and strategic sourcing can transform a complex corporate structure into a truly passive, high-yield investment.

The Shifting Landscape of UK Property: Why Incorporation Dominates 2026

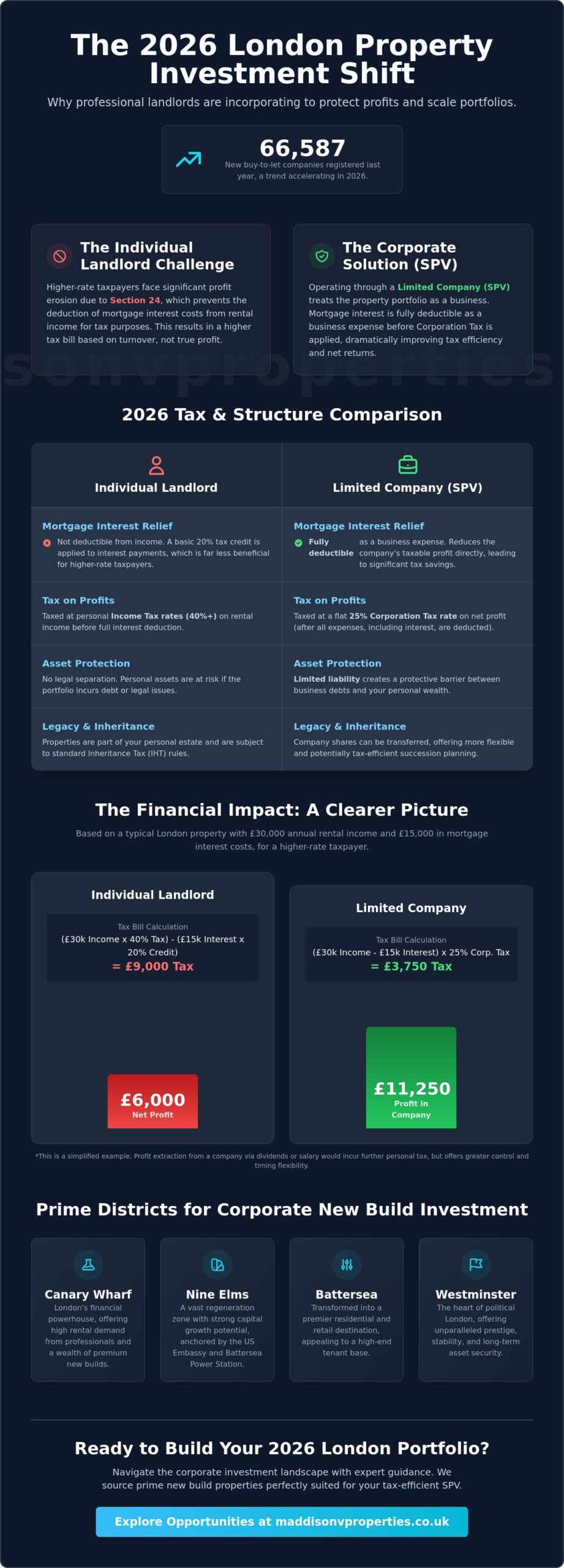

The era of the casual property owner is over. For years, individual landlords have grappled with the restrictive legacy of Section 24, which prevents higher-rate taxpayers from deducting mortgage interest from their rental income. By mid-2026, this tax burden has reached a critical breaking point, forcing a fundamental rethink of how wealth is preserved in the capital. Professional investors now view their holdings not as personal assets, but as a sophisticated corporate enterprise. This shift mirrors the structural stability seen in major entities like British Land, where corporate governance provides a shield against personal tax volatility and creates a foundation for genuine scale.

Current market sentiment reflects this professionalization with striking clarity. Data from 2025 showed a record 66,587 new buy-to-let companies registered in the UK, a trend that has only accelerated into the current year. When you’re financing a property portfolio within a limited company, you’re choosing a path of resilience and scalability that individual ownership simply cannot match. It’s a strategy designed for the ambitious investor who values financial security, order, and effortless oversight.

To better understand the practical steps of this corporate transition, watch this helpful video:

The Death of the Accidental Landlord

Individual ownership is becoming increasingly unsustainable for those in the higher tax brackets. The transition toward a business-first mindset isn’t just about tax; it’s about adopting a rigorous, professional approach to asset management. At MaddisonV, we help clients navigate this shift by connecting them with expert property sourcing agents London who understand the specific requirements of corporate acquisitions. We ensure that every property added to your portfolio aligns with the high standards expected by modern corporate lenders, focusing on quality and long-term capital appreciation.

The Rise of the Professional SPV

A Special Purpose Vehicle (SPV) is a limited company created solely for property investment. Lenders overwhelmingly prefer this structure over general trading companies because it ring-fences the property assets from other business risks. When incorporating, the use of specific SIC codes, such as 68209 for the letting and operating of own or leased real estate, is vital. It signals to financial institutions that the company is a clean, dedicated vehicle for financing a property portfolio within a limited company. This clarity simplifies the application process and provides the stability needed for long-term growth. By utilizing a dedicated SPV, you ensure that your personal finances remain separate from your investment liabilities, creating a clean, rhythmic approach to wealth building.

The Financial Architecture: Tax Efficiency and Asset Protection

The financial architecture of a modern investment strategy rests on three primary pillars: efficiency, protection, and legacy. When you’re financing a property portfolio within a limited company, you replace the unpredictable volatility of personal tax changes with a stable, business-oriented framework. This structure allows you to treat every pound of rental income with surgical precision, ensuring that your capital remains within your control rather than being diluted by the onerous personal levies that often plague individual landlords in 2026.

The core advantage of this model is the legal separation it provides. By housing your assets within a Special Purpose Vehicle, you create a robust barrier between your personal life and your professional investments. This separation ensures your family home and personal savings remain protected from property-related liabilities, offering a level of mental tranquility that is essential for long-term peace of mind. It’s a sophisticated, secure, and prestigious way to manage significant wealth in the capital’s competitive market.

Mastering the Corporation Tax Advantage

In the 2026/2027 tax year, the corporate landscape offers a clear tiered structure for profitability. According to the official government overview of Corporation Tax, companies with profits of £50,000 or less benefit from a 19% small profits rate, while those exceeding £250,000 are subject to a 25% main rate. Marginal relief provides a smooth transition for those in between, but the true power lies in full mortgage interest deductibility. Unlike individual owners who face Section 24 restrictions, a limited company can deduct 100% of its mortgage interest as a business expense before tax is even calculated.

In 2026, the ability to reinvest gross rental profits directly into new acquisitions without the erosion of personal income tax creates a powerful compounding effect that accelerates portfolio growth. Furthermore, dividend flexibility allows you to control your personal tax threshold with ease. With a £500 dividend allowance and tiered rates for basic, higher, and additional rate taxpayers, you can time your withdrawals to align with your broader financial goals. For those seeking to optimize these complex flows, our team provides bespoke portfolio management to ensure every asset performs at its peak.

Inheritance Tax and Family Legacy Planning

A corporate structure is more than just a tax vehicle; it’s a tool for generational wealth transfer. By utilizing share structures, you can gradually transfer ownership to family members without losing control of the underlying assets. Alphabet shares allow for bespoke dividend distributions tailored to each family member’s tax position, making the company a flexible family investment vehicle. This arrangement simplifies the eventual transfer of a portfolio, avoiding the disruptive costs and complexities of selling properties individually to settle inheritance tax liabilities. It’s a fluid, orderly, and comprehensive approach to building a lasting legacy in London’s most desirable districts.

Individual vs. Limited Company: A 2026 Strategic Comparison

Choosing between personal ownership and a corporate structure is a pivotal moment in an investor’s journey. It’s a decision that requires a clear-eyed analysis of your long-term wealth objectives. While the tax benefits of financing a property portfolio within a limited company are substantial, they must be balanced against the higher operational costs of running a business. Professional investors view these costs as a necessary investment in a structure that offers superior protection, scalability, and order. It’s about moving from a reactive mindset to a proactive, business-first strategy that prioritizes long-term stability over short-term simplicity.

The “Smart Money” approach in 2026 favors incorporation for those targeting high-value London districts. When you’re managing assets in Westminster or Battersea, the administrative burdens of accountancy fees and Companies House filings are dwarfed by the potential for tax-efficient growth. The break-even point for most investors occurs when they enter the higher tax bracket or when their portfolio expands beyond a single asset. At this stage, the ability to retain and reinvest profits within the company becomes mathematically superior to personal ownership, where the 40% or 45% tax rate significantly hampers capital accumulation.

The Mortgage Landscape for 2026 SPVs

Lenders have increasingly refined their offerings for Special Purpose Vehicles, narrowing the gap between individual and corporate products. In June 2026, representative five-year fixed rates for limited companies sit at approximately 5.49% with no fee at 75% LTV. For those seeking shorter terms, two-year fixed rates are available around 4.39% with a 3% fee. These products are particularly accessible for new build developments, where high LTV options remain robust. Given the complexity of these structures, seeking a bespoke buy-to-let mortgage guide consultation is essential to secure terms that align with your specific cash flow requirements and lifestyle goals.

Capital Gains and the Incorporation Relief Debate

Transferring an existing personal portfolio into a company remains a significant hurdle due to the friction of Capital Gains Tax and Stamp Duty Land Tax. With a 5% SDLT surcharge on additional properties and corporate acquisitions, the cost of moving assets can be prohibitive. For higher-rate taxpayers, the individual CGT rate on residential property stands at 24%, making a transfer a costly endeavor even with potential incorporation relief. This is why many sophisticated investors choose to start fresh by purchasing new build properties directly through their SPV. Buying new in growth districts like Nine Elms is a cleaner, more efficient way to build a corporate portfolio without the tax baggage of legacy personal holdings. It allows for a fluid transition into a professional structure that is designed for the future, not the past.

Incorporating for Prime London: New Builds and High-Growth Districts

The strategic decision to house your assets in a corporate structure is only half the battle; the other half is selecting locations that can withstand the scrutiny of institutional lenders. In 2026, the synergy between a professional corporate vehicle and high-value London districts has become the hallmark of a sophisticated investor. Financing a property portfolio within a limited company is most effective when paired with assets that offer both capital resilience and high rental demand. Districts like Nine Elms, Battersea, and Canary Wharf provide the perfect backdrop for this model, offering the high-end aesthetics and functional standards that modern tenants and corporate lenders require.

By focusing on these growth corridors, you align your investment with the city’s evolving infrastructure. This alignment ensures that your company’s balance sheet remains robust, reflecting the prestige and stability of the capital’s most ambitious developments. It is a fluid, orderly, and comprehensive approach to wealth building that minimizes risk while maximizing long-term rewards.

Geographic Strategy: Canary Wharf and Nine Elms

Nine Elms and Battersea have matured into premier choices for corporate holding, offering significant potential for capital growth as the area’s regeneration reaches its final, most prestigious phases. These districts attract a high-caliber demographic that values the lifestyle benefits of modern, professionally managed environments. Similarly, Canary Wharf remains a staple for professional corporate portfolios. Its established rental market and proximity to global financial hubs ensure a steady, rhythmic flow of income that is vital for servicing corporate debt. For those looking toward the heart of the city, luxury acquisitions in Westminster offer a timeless appeal, providing a level of asset protection that is highly prized by high-net-worth corporate structures.

The Operational Edge of New Builds

New build property offers a distinct operational edge that simplifies the administration of a limited company. Lower maintenance costs translate directly into cleaner corporate balance sheets, as the need for significant sinking funds is greatly reduced. Most developments come with 10-year warranties, providing a layer of financial security that alleviates the anxieties typically associated with aging assets. This predictability is essential for maintaining the mental tranquility and professional distance that a passive investment structure promises.

In the 2026 Green regulatory environment, energy efficiency has become a critical factor for mortgage eligibility. New builds consistently achieve EPC ratings of B or higher, positioning them perfectly for future green mortgage incentives and lower interest rates. This foresight ensures your portfolio remains compliant and competitive as environmental standards tighten. To explore how these high-performance assets can be integrated into your strategy, we invite you to view our latest off-plan investment opportunities across London’s most desirable growth districts.

Building Your 2026 Portfolio with MaddisonV

Scaling a sophisticated property portfolio in 2026 requires more than just capital; it demands a partner who understands the intricate mechanics of corporate ownership. At MaddisonV Properties, we bridge the gap between clinical asset management and a genuine appreciation for high-quality environments. We recognize that financing a property portfolio within a limited company is a strategic choice made by ambitious investors who value their time as much as their returns. Our role is to handle the complex operational details, allowing you to enjoy the rewards of your investment with complete mental tranquility.

Our end-to-end advisory service begins long before a contract is signed. We provide comprehensive mortgage consultations tailored to the unique requirements of SPVs, ensuring your financing structure is as robust as the assets themselves. By positioning ourselves as a premium partner, we offer an aspirational experience that transforms property ownership into a fluid, effortless process. It’s a journey defined by reliability, prestige, and a meticulous attention to detail.

Bespoke Sourcing for Corporate Investors

We use a rigorous set of criteria to identify what we call Company-Ready assets. These are properties in high-growth districts like Canary Wharf and Nine Elms that meet the exacting standards of corporate lenders and high-tier tenants. A significant part of our strategy involves off-plan property investment, where meticulous due diligence is paramount to securing long-term capital appreciation. Our deep-rooted industry connections provide our clients with exclusive access to off-market opportunities, ensuring you’re always ahead of the broader market and positioned within London’s most resilient neighborhoods.

Effortless Management and Facilities Oversight

The administrative weight of being a corporate landlord can be onerous, but our professional property management and facilities management services alleviate this burden entirely. We maintain the visual and functional standards of your portfolio with a detail-oriented style that suggests nothing is left to chance. From overseeing luxury developments in Battersea to managing high-yield units in Westminster, we ensure your assets retain their prestige and value over time. We handle the tenant relations, the regulatory filings, and the physical upkeep so your involvement remains purely strategic.

This passive partnership approach is designed for those who wish to outsource significant responsibilities to a trusted expert. We invite you to book a consultation with our team to develop a tailored 2026 investment strategy that aligns with your vision for financial security and family legacy. Let us handle the complexities of financing a property portfolio within a limited company while you focus on the rewards of a professionally curated London portfolio.

Charting a Course for Generational Wealth

The shift toward professional incorporation represents more than just a tax strategy; it’s a commitment to building a resilient and scalable legacy. By moving away from individual ownership, you embrace a structure that offers superior financial security, asset protection, and operational order. This approach is particularly powerful when applied to the capital’s most prestigious new build developments, where energy efficiency and high rental demand provide a stable foundation for growth.

At MaddisonV, we specialize in the unique demands of the London market. Our expertise as specialists in Canary Wharf and Nine Elms new builds ensures you have access to the most promising opportunities. We provide a bespoke mortgage advisory for SPV structures and comprehensive facilities management for luxury portfolios, handling the intricate details so you can enjoy the rewards of a truly passive investment. Financing a property portfolio within a limited company doesn’t have to be complex when you have a premium partner by your side.

Secure your 2026 London investment strategy with a MaddisonV consultation. Your journey toward a more secure and sophisticated property future starts today.

Frequently Asked Questions

Is a limited company better for buy-to-let in 2026?

For higher-rate taxpayers, a limited company is often the superior choice in 2026. This structure bypasses Section 24 restrictions, allowing you to deduct mortgage interest from your rental income before tax is calculated. It’s particularly effective for those focused on reinvesting profits to scale their holdings. You should evaluate your specific tax bracket and long-term goals to ensure the administrative costs align with your financial objectives.

How much does it cost to set up a property SPV?

Setting up a property SPV is relatively inexpensive at the point of registration. While Companies House fees are minimal, you’ll need to budget for professional legal and accountancy support to ensure your articles of association meet lender requirements. The true cost lies in the ongoing administration, such as annual accounts and corporation tax filings. These expenses are a necessary investment in a structure that provides long-term financial security and order.

Can I transfer my personal mortgage to a limited company?

You cannot simply transfer a personal mortgage to a limited company. The process is legally treated as a sale from you to your company, requiring a new mortgage application in the company’s name. This transaction triggers Capital Gains Tax and Stamp Duty Land Tax based on the property’s current market value. Most investors find that financing a property portfolio within a limited company is most efficient when starting with new acquisitions.

Do I pay more Stamp Duty when buying through a limited company?

Yes, buying through a limited company generally incurs a higher rate of Stamp Duty Land Tax. Companies are subject to the 5% surcharge on all residential property purchases in England and Northern Ireland as of June 2026. While this increases the initial acquisition cost, many professional investors view it as a manageable expense when weighed against the significant corporation tax advantages and long-term asset protection that the corporate structure provides.

What is the Special Purpose Vehicle (SPV) for property?

A Special Purpose Vehicle (SPV) is a limited company formed exclusively for property investment. By using a dedicated vehicle with the correct SIC code, such as 68209, you provide lenders with the transparency they require. This structure ring-fences your property assets from other business risks, ensuring a high level of stability. It’s a clean, rhythmic way to manage a professional portfolio while maintaining a clear distance between your personal and business liabilities.

Can I use a limited company for off-plan property in London?

Yes, using a limited company for off-plan property in London is a highly effective strategy for 2026. It allows you to secure high-quality assets in districts like Nine Elms or Canary Wharf from the outset within a tax-efficient vehicle. This approach avoids the friction of moving properties into a company later. It’s a sophisticated way to build a portfolio of new build properties that meet modern energy standards and attract premium tenants.

How do I pay myself from a property limited company?

You can extract income from your company through a combination of salary and dividends. Most directors utilize a small salary to maintain their National Insurance record and take the remainder as dividends to benefit from the lower tax rates. Strategic dividend planning allows you to control your personal tax exposure with precision. This flexibility is a cornerstone of the professionalized approach to financing a property portfolio within a limited company, offering both efficiency and peace of mind.

Are mortgage rates higher for limited companies than individuals?

Mortgage rates for limited companies have historically been higher, but the gap has narrowed significantly by mid-2026. Lenders have become more comfortable with SPV structures, leading to a more competitive market. While you might pay slightly more in interest or arrangement fees compared to a personal mortgage, the ability to offset 100% of that interest against your rental income often results in a higher net return for professional investors.

Sign Up Now

Want to read more great articles and blogs subscribe to our newsletter