Did you know that prime apartment prices in Dubai remain approximately 64% cheaper per square meter than equivalent properties in London? While the...

Did you know that prime apartment prices in Dubai remain approximately 64% cheaper per square meter than equivalent properties in London? While the financial allure is undeniable, the logistical leap from the Thames to the Arabian Gulf often feels daunting for British investors. You likely recognize that financing property in dubai from uk requires more than just a healthy balance sheet; it demands a strategic bridge between UK financial standards and UAE lending regulations. We understand the hesitation that comes with shifting currency values, complex income verification, and the substantial deposit requirements typical of international transactions.

This guide empowers you to master the nuances of cross-border lending so you can secure high-leverage financing with absolute confidence. You’ll learn how to navigate the 2026 market of interest rates, loan-to-value ratios, and the total cost of acquisition. We explore the pathways to securing premium leverage, managing the relationship between GBP and AED, and ensuring your new asset remains a source of effortless, passive wealth. Our roadmap provides the clarity, security, and professional distance you need to expand your portfolio into one of the world’s most ambitious real estate markets.

Key Takeaways

- Confirm your legal eligibility as a UK resident to access UAE-regulated lending and understand why Dubai remains a premier diversification target in 2026.

- Master the specific income thresholds and LTV requirements for financing property in dubai from uk to ensure your application is both robust and competitive.

- Evaluate the strategic advantages of developer-led payment structures for off-plan investments versus traditional mortgage valuations for ready properties.

- Navigate the administrative journey with confidence, from securing an initial Approval in Principle to finalising registration with the Dubai Land Department.

- Learn how to transition from a successful acquisition to a high-yield asset through professional sourcing and sophisticated portfolio management.

Understanding the 2026 Landscape: Can UK Residents Finance Dubai Real Estate?

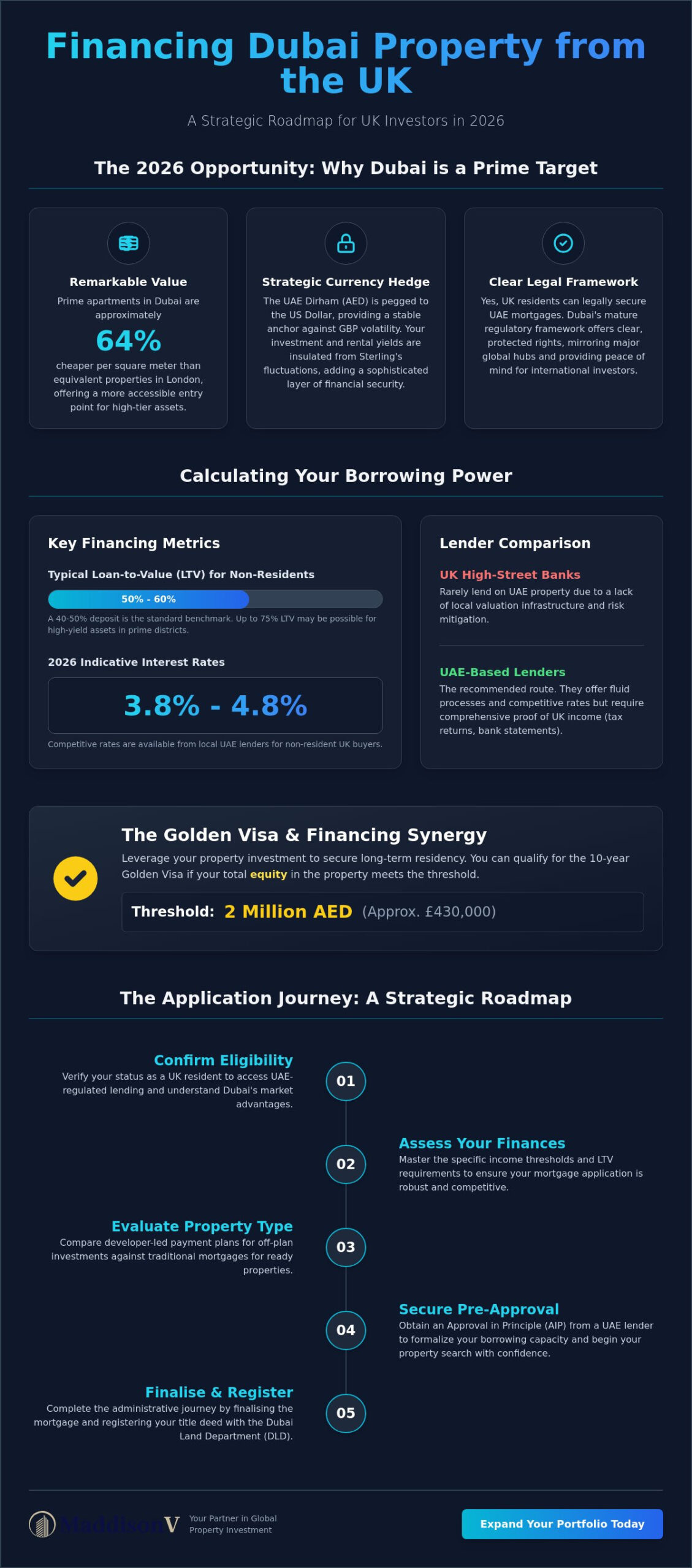

British investors often ask if they’re legally permitted to hold debt in the Emirates while residing in the UK. The answer is a definitive yes. In 2026, the regulatory framework surrounding Dubai’s real estate market has reached a level of maturity that mirrors major global hubs, offering UK citizens clear, protected rights to secure UAE mortgages. As London investors seek to diversify away from domestic tax pressures and cooling yields in the capital, Dubai has emerged as a primary target for capital preservation and growth. With property prices in Dubai remaining approximately 64% cheaper per square meter than in London, the entry point for high-tier assets is remarkably accessible.

A strategic advantage often overlooked by competitors is the currency hedge provided by the United Arab Emirates. Because the UAE Dirham (AED) is pegged to the US Dollar, your investment acts as a stable anchor against the historical volatility of the British Pound. When you’re financing property in dubai from uk, you aren’t just buying bricks and mortar; you’re positioning your capital in a dollar-denominated environment. This provides a sophisticated layer of financial security, ensuring that your rental yields and capital appreciation are insulated from Sterling’s fluctuations. For a deeper look at the broader market dynamics, you can explore our comprehensive guide to invest in dubai property.

To better understand this concept, watch this helpful video:

UK Banks vs. UAE Banks: Where to Source Your Loan

UK high-street banks rarely lend on UAE collateral because they lack the local valuation infrastructure to mitigate risk. While some international private banks in London offer bespoke solutions for ultra-high-net-worth individuals, most investors find that local UAE lenders provide more fluid processes. Using a UAE bank as a non-resident allows you to access competitive interest rates, which currently range between 3.8% and 4.8% for 2026. However, you’ll need to prepare for stricter documentation; UAE banks require comprehensive proof of UK income, including tax returns and certified bank statements, to satisfy their underwriting criteria.

The Golden Visa and Financing Synergy

Your financing strategy should align with your long-term residency goals. In 2026, the threshold for the 10-year Golden Visa remains at 2 million AED, which is approximately £430,000. If you’re financing property in dubai from uk, you can still qualify for this visa as long as your total equity in the property meets the 2 million AED mark. This creates a powerful synergy for investors; you can leverage a mortgage to acquire a higher-value asset in a prime district like Downtown Dubai or the Palm Jumeirah, while simultaneously securing long-term residency rights. This dual approach establishes a foundation of personal and financial security in one of the world’s most ambitious cities.

Calculating Your Borrowing Power: LTV Ratios and Income Requirements

Securing leverage as an international investor requires a clear-eyed understanding of how UAE lenders perceive risk. While the process is streamlined, financing property in dubai from uk involves different parameters than a standard London buy-to-let. In 2026, non-resident investors should expect Loan-to-Value (LTV) ratios between 50% and 60%. Some premier lenders may extend to 75% for high-yield assets in prime districts, but a 40% to 50% deposit remains the standard benchmark for security. This conservative approach reflects the current climate of foreign investment in Dubai real estate, where stability is prioritized over aggressive lending.

Age limits also play a critical role in your borrowing power. Unlike the UK, where mortgage terms can often extend into retirement, UAE banks typically enforce a strict exit age of 65 for salaried employees and 70 for the self-employed. This means a 50-year-old investor may only be eligible for a 15-year term. This shortened window directly impacts monthly cash flow and requires a more robust repayment strategy. Regarding collateral, you cannot cross-collateralize UK property against a UAE loan. The Dubai asset must stand on its own financial merit, ensuring a clean separation between your domestic and international portfolios.

Non-Resident LTV vs. Resident LTV

The gap between resident and non-resident leverage remains a defining factor for UK buyers. Residents often access up to 80% LTV, while you’ll likely be capped at 60% as a non-resident. To bridge this, many sophisticated clients use a ‘Cash-Plus-Mortgage’ strategy, putting down a 40% deposit to secure a premium luxury apartment. If you eventually obtain residency through the Golden Visa program, you can often refinance to unlock higher leverage. If you’re unsure how these ratios affect your specific budget, our Mortgage Consultations can provide a tailored breakdown of your borrowing capacity.

Proving UK Income to UAE Underwriters

UAE banks demand meticulous documentation to verify your UK-based earnings. Salaried employees must provide three to six months of payslips and their latest P60, while entrepreneurs and the self-employed require two years of audited accounts. Interestingly, lenders often view UK rental income as a secondary source of funds. This can bolster your application significantly. A clean UK credit report is non-negotiable. UAE underwriters use this as a primary gauge of your global financial character and reliability. They look for stability, order, and a consistent history of meeting financial obligations.

Financing Off-Plan vs. Ready Properties in Dubai’s Prime Districts

The choice between a completed residence and a future development is a fundamental strategic decision that shapes your entire capital commitment. When financing property in dubai from uk, the route you choose dictates your initial cash outlay and your immediate rental potential. For ready properties, the process mirrors the UK secondary market, requiring a formal bank valuation and a traditional mortgage structure. In 2026, these valuations are increasingly rigorous, ensuring that the loan amount aligns perfectly with the asset’s current market standing. This provides a layer of security for the investor, confirming that the high-leverage financing is supported by tangible, existing value.

Conversely, the appeal of off-plan acquisitions lies in the flexibility of the financial commitment. While traditional banks typically only offer mortgages once a project has reached 50% completion, developer-led payment plans have become the sophisticated alternative to institutional lending. These structures allow you to secure a premium asset with a series of interest-free installments tied to construction milestones. This approach is particularly effective for those looking to manage liquidity without the immediate pressure of monthly interest payments. To understand the full scope of these opportunities, explore our detailed guide to off-plan property investment.

Developer Payment Plans: The Mortgage Alternative

Post-handover payment plans are a unique feature of the UAE market that provide immense value to British investors. These plans allow you to pay a portion of the purchase price over several years after you have already taken possession of the property. It’s essentially interest-free credit, allowing the property’s own rental yield to contribute toward the remaining balance. We ensure that every developer we partner with maintains strict escrow compliance. This means your funds are held in a government-regulated account, providing the peace of mind that your capital is protected, managed, and utilized solely for the project’s completion.

District Spotlight: Sourcing High-Yield Assets

Applying London-style sourcing logic to Dubai reveals clear parallels for the discerning investor. Business Bay and Dubai Marina function much like Canary Wharf and Battersea; they are high-growth hubs defined by professional demand and premium aesthetics. Many investors who traditionally focused on Westminster are now pivoting to Dubai Creek Harbour, attracted by its promise of modern prestige and superior capital appreciation. Whether you are financing a high-rise apartment in Downtown Dubai or a luxury villa in “The Valley”, the district you choose dictates the lending appetite. Banks often provide more favorable terms for properties in established, prime locations where liquidity is high and demand is constant.

The Application Journey: A Strategic Roadmap for UK Investors

Success in the Dubai market is built on preparation rather than reaction. When you’re financing property in dubai from uk, your journey must begin with an Approval in Principle (AIP). This document is your financial passport; it confirms your borrowing capacity and signals to sellers that you’re a serious, pre-qualified buyer. Without an AIP, you risk losing prime assets in fast-moving districts to investors who have already solidified their lending position. Once your AIP is in hand, the search moves to the Memorandum of Understanding, commonly known as “Form F.” This is the legally binding contract between buyer and seller that outlines the price, timelines, and contingencies of the transaction.

The Dubai Land Department (DLD) serves as the ultimate arbiter of property rights, overseeing the mortgage registration and the final transfer of title. Unlike the UK’s sometimes protracted conveyancing process, Dubai transactions can complete in as little as two to four weeks if the documentation is in order. The final drawdown involves a coordinated transfer of funds from your UK accounts to the UAE. We manage these complexities with meticulous care, ensuring that currency exchange and international bank transfers are timed perfectly to meet DLD deadlines. This rhythmic, orderly approach transforms a complex cross-border transaction into a fluid and predictable experience.

Documentation and Attestation

The “Apostille” process is where many self-managed applications falter. UAE banks require UK-issued documents, such as marriage certificates or audited accounts, to be legalised for use in the Emirates. This involves a multi-step journey: verification by a UK solicitor, attestation by the Foreign, Commonwealth & Development Office (FCDO), and final legalisation by the UAE Embassy in London. Certified translations into Arabic may also be required for certain lenders. A No Objection Certificate (NOC) is a formal document issued by the developer confirming that all service charges have been settled and they have no objection to the property’s title being transferred to a new owner.

The Role of a Specialist Sourcing Agent

Identifying a property is only the first step; ensuring it is “bankable” is where our expertise becomes invaluable. MaddisonV Properties focuses on assets that meet the strict valuation criteria of UAE lenders, protecting you from properties with inflated price tags or legal encumbrances. Our team negotiates directly with developers to align their payment plans with your specific financing needs, creating a bespoke strategy that maximises your liquidity. We apply the same rigorous methodology found in our guide to property sourcing agents London to the Dubai market, ensuring every acquisition is a high-yield, secure investment. To begin your journey with a partner who understands the nuances of international lending, explore our Mortgage Consultations today.

Maximising ROI: How Professional Sourcing and Financing Synergy Works

Securing high-leverage capital through financing property in dubai from uk represents the foundation of a successful venture, yet the true yield is realized in the operational phase. While the initial mortgage structure provides the entry point, the long-term appreciation of your asset depends on a seamless transition from acquisition to professional oversight. We believe that an investor’s involvement should remain entirely passive, allowing the rewards of your international portfolio to accumulate without the burden of daily logistical hurdles. This professional distance ensures that your capital works for you, rather than you working for your capital.

The MaddisonV Properties approach integrates bespoke sourcing, strategic financing, and rigorous facilities management into a single, cohesive experience. By aligning your debt structure with a comprehensive management plan, you ensure that the property remains a “bankable” asset throughout its lifecycle. This integrated strategy is vital for maintaining your equity position during future refinancings or portfolio expansions. When an asset is curated and managed to a premium standard, it attracts discerning tenants and preserves its capital value, ensuring your financial security is never left to chance.

Integrated Property and Facilities Management

Maintaining a desert-based asset from the UK requires a partner who understands the unique environmental and regulatory demands of the Emirates. Effective property management acts as the bridge between a vacant unit and a high-performing investment. MaddisonV Properties utilizes dedicated facilities management teams to focus on maintaining high-end aesthetics and functional standards. This proactive oversight is essential for tenant retention and consistent yields, protecting your initial investment from the accelerated wear often seen in the Gulf’s climate.

This level of specialized care is universal for properties in high-temperature zones; for example, homeowners in heat-intensive regions like Florida rely on Ultra Air Heating and Cooling for the technical expertise needed to ensure climate control systems remain efficient under extreme conditions.

Expanding Your Global Portfolio

Many of our most successful clients use the robust, tax-free yields from their Dubai assets to finance further acquisitions within the UK. This “London-Dubai Bridge” allows you to leverage the high-yield environment of the Emirates alongside the long-term capital stability of real estate in england london. Whether you’re looking to reinvest in a new build property in Canary Wharf or a heritage asset in Westminster, MaddisonV Properties provides a holistic, multi-jurisdiction investment plan. This unified vision ensures your global interests are diverse, secure, and positioned for maximum growth.

Secure Your Global Investment Legacy in 2026

Mastering the nuances of financing property in dubai from uk is the final step in establishing a truly global, resilient portfolio. We’ve navigated the transition from UK-regulated advisory to UAE-regulated lending, highlighting the importance of the Approval in Principle and the strategic advantage of the AED/USD peg. By understanding the interplay between high-leverage financing and professional management, you’ve gained the roadmap necessary to expand your interests beyond the London market into one of the world’s most ambitious real estate landscapes. This journey isn’t just about acquisition; it’s about securing a dollar-denominated future with absolute clarity.

MaddisonV Properties provides the air of quiet confidence required to bridge these two major financial hubs with ease. As specialists in high-growth Dubai and London new builds, we offer the end-to-end expertise in cross-border regulations that ensures your capital remains secure and your involvement remains passive. Your path to international wealth is now clear, supported by a partner committed to your long-term financial security and aesthetic standards. Book Your Bespoke Dubai Financing Consultation with MaddisonV Properties and begin your next chapter of investment excellence today.

Frequently Asked Questions

Can I get a mortgage in British Pounds (GBP) for a Dubai property?

You cannot typically secure a mortgage in British Pounds for a Dubai property through a UAE lender. Mortgages are issued in UAE Dirhams (AED) to align with the local currency and property valuation standards. This ensures your debt and asset value remain in the same currency, simplifying your financial planning and reducing immediate exchange rate risks during the repayment term.

What is the minimum deposit required for a UK resident buying in Dubai?

UK residents should expect a minimum deposit requirement of 40% to 50% of the property’s purchase price. While residents in the UAE can access higher leverage, non-resident investors are generally capped at a 50% to 60% Loan-to-Value (LTV) ratio. This ensures a stable equity cushion and reflects the conservative lending standards maintained by UAE financial institutions for international clients.

Do I need to travel to Dubai to sign my mortgage documents?

You don’t necessarily need to travel to Dubai to finalise your mortgage. Many UK investors utilize a Power of Attorney (POA) to allow a legal representative or sourcing agent to sign documents on their behalf. The process is increasingly digital, allowing for remote transactions that maintain high standards of security, efficiency, and professional distance without requiring your physical presence.

How does the AED/USD peg benefit UK-based property investors?

The AED/USD peg provides a sophisticated hedge against the historical volatility of the British Pound. Because the Dirham is fixed to the US Dollar, your investment in Dubai real estate serves as a stable, dollar-denominated asset. This offers a layer of financial security and capital preservation that is highly valued by investors looking to diversify away from Sterling-based risks.

Can I use my UK rental income to qualify for a UAE mortgage?

You can use your UK rental income to strengthen your application when financing property in dubai from uk. UAE banks typically accept documented rental earnings as a secondary source of funds, provided you can present certified bank statements and valid tenancy agreements. This additional liquidity can be the deciding factor in securing more competitive terms or a higher loan amount.

Are there specific UK tax implications for financing a Dubai property?

While Dubai has no annual property or income tax, you must remain mindful of your UK tax obligations. As a UK tax resident, your worldwide income, including rental yields from Dubai, is generally subject to UK Income Tax. We recommend consulting with a qualified tax professional to understand how your international debt and income will interact with your domestic tax profile and personal allowances.

What are the typical mortgage interest rates in Dubai for 2026?

For 2026, mortgage interest rates for non-resident UK buyers typically range between 3.8% and 4.8%. These rates can be fixed for an initial period or variable based on the EIBOR (Emirates Interbank Offered Rate). Securing these competitive figures requires a robust financial profile and a clear demonstration of stable, UK-based earnings to satisfy the local underwriting criteria.

Can I finance a Dubai property through a UK Limited Company?

Financing a Dubai property through a UK Limited Company is complex and rarely supported by standard UAE retail banks. Most lenders prefer lending to individuals or specifically structured UAE Special Purpose Vehicles (SPVs). If your strategy requires corporate ownership, establishing a local holding structure is often the more fluid, bankable, and legally sound path to securing high-leverage financing.

Sign Up Now

Want to read more great articles and blogs subscribe to our newsletter