For the discerning London investor, holding prime assets in your own name is no longer a simple default; it's often a quiet compromise on your future...

For the discerning London investor, holding prime assets in your own name is no longer a simple default; it’s often a quiet compromise on your future wealth. You’ve likely watched your rental yields in Canary Wharf or Battersea diminish under the weight of high personal income tax and the restrictive reach of Section 24. Understanding the specific tax implications of buying property in a company name uk has become essential for those seeking to maintain a high-quality, profitable portfolio in a shifting regulatory environment. It’s a common frustration to feel that your hard-earned investments are being squeezed by rules that overlook the nuances of professional property ownership.

We’re here to help you navigate this corporate landscape to maximise tax efficiency, ensure portfolio scalability, and protect your family legacy. This 2026 guide provides a clear look at the current 25% Corporation Tax main rate, the updated 5% Stamp Duty surcharge, and the strategic reliefs available for high-value developments in Nine Elms or Westminster. You’ll discover a sophisticated framework for asset protection that offers mental tranquility, financial order, and long-term prestige. We’ll explore how a structured corporate approach handles the complex details so you can enjoy the rewards of a truly professional investment strategy.

Master the transition from personal to corporate ownership to unlock superior tax efficiency, portfolio scalability, and full mortgage interest deductibility for your London assets. This guide provides a meticulous analysis of the tax implications of buying property in a company name uk, offering clarity on the 2026 Corporation Tax rates and the 5% Stamp Duty surcharge. You’ll learn how to manage ATED compliance for properties over £500,000, ensuring your Property Investment remains compliant, secure, and profitable.

We explore the strategic advantages of focusing on high-growth districts like Canary Wharf, Nine Elms, and Battersea, where a New Build Property provides the ideal foundation for a sophisticated corporate SPV. Discover how a professional partnership handles the complexities of corporate compliance, facilities management, and portfolio oversight, ensuring your investment journey is effortless, secure, and truly aspirational. By the end of this guide, you’ll have the knowledge to protect your wealth and build a lasting investment legacy that serves your family for generations.

Understanding the Shift: Personal vs. Corporate Property Ownership

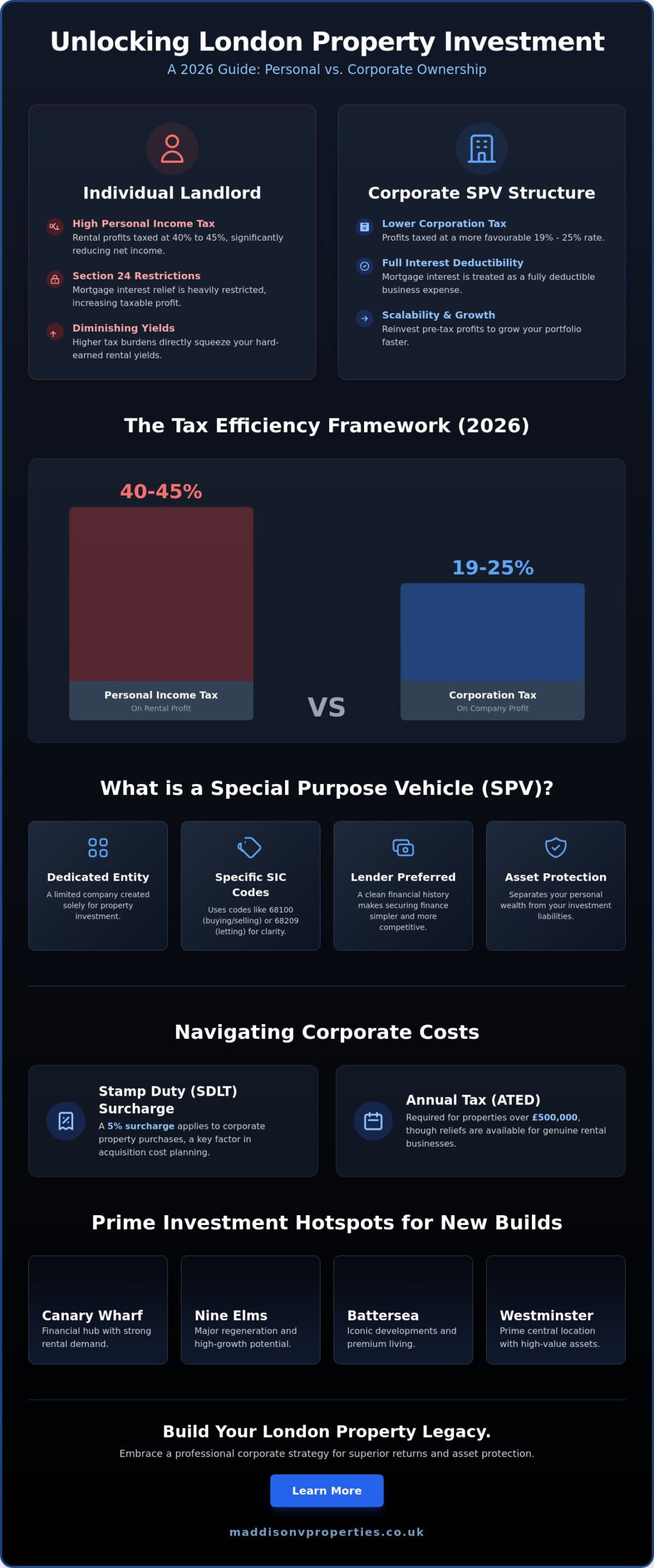

Shifting from individual ownership to a corporate framework represents a fundamental shift in how sophisticated wealth is managed. For years, the “Individual Landlord” model was the standard path for those acquiring London assets. However, the implementation of Section 24 changed the equation by restricting mortgage interest relief for private owners. This legislation effectively turned a gross profit into a net loss for many higher-rate taxpayers, making the tax implications of buying property in a company name uk a critical consideration for 2026. By moving to a corporate structure, you treat your portfolio as a business rather than a personal hobby, allowing for a more rhythmic and predictable growth pattern that prioritizes long-term stability.

To better understand how this transition works in practice, watch this helpful video:

What is an SPV and Why Does it Matter?

A Special Purpose Vehicle, or SPV, is a limited company created for the sole purpose of property investment. Lenders generally prefer this structure over a standard trading company because it provides a clean financial history, free from the complexities of other business liabilities. By using specific Standard Industrial Classification (SIC) codes, such as 68100 for buying and selling or 68209 for letting, you signal to banks that your entity is a dedicated vehicle for real estate. This focus helps in securing more competitive mortgage rates and simplifies the process of sourcing high-end off-plan opportunities in high-value districts like Westminster or Nine Elms. It offers a layer of asset protection that keeps your personal liabilities separate from your professional ventures, ensuring that your investment legacy remains secure and distinct.

Regulatory Shifts and the 2026 Landscape

Regulatory shifts in 2026 mark a pivotal point for restructuring, as the UK corporation tax rates and filing requirements have reached a state of settled maturity. HMRC now views corporate transparency not as a burden, but as a marker of prestige and reliability for serious investors. Professional owners understand that meticulous compliance is the price of scalability. While the main corporation tax rate remains at 25% for profits over £250,000, the ability to fully deduct mortgage interest remains a unique advantage of the corporate model. Analyzing the tax implications of buying property in a company name uk ensures that your investment remains a source of mental tranquility rather than administrative anxiety. Working with expert advisory ensures your structure remains fluid, efficient, and ready for future acquisitions in Canary Wharf or Battersea. It’s about creating a legacy that is both aesthetically pleasing in its growth and grounded in high-tier standards of financial order.

The Core Tax Advantages of a Limited Company Structure

Choosing a corporate structure transforms your tax liability from a personal burden into a manageable business expense. For high-rate taxpayers, the difference between personal income tax rates of 40% or 45% and the current Corporation Tax rates is substantial. Companies with profits up to £50,000 benefit from a 19% rate, while those exceeding £250,000 are capped at 25%. This delta allows you to retain a larger portion of your rental yields within the company envelope. Reinvesting these “pre-tax” profits is a powerful engine for growth, especially when targeting high-value developments in Canary Wharf or Battersea. Understanding these tax implications of buying property in a company name uk is the first step toward building a truly scalable investment vehicle.

Maximising Mortgage Interest Relief

The most compelling reason to analyze the tax implications of buying property in a company name uk remains the treatment of finance costs. Individual landlords are restricted to a 20% tax credit, which often results in paying tax on phantom profits even if their actual cash flow is negative. In contrast, a limited company treats mortgage interest as a fully deductible business expense. This means you only pay tax on the profit remaining after all interest payments are settled. Full corporate mortgage interest relief effectively lowers the net cost of prime London financing by allowing interest to be deducted before the tax liability is calculated. This structural advantage significantly improves cash flow for leveraged properties in premium districts like Nine Elms, where financing costs can be a major factor.

Dividend Strategies and Wealth Extraction

Extracting wealth from a company requires a sophisticated touch to remain tax-efficient. Professional investors often utilize a bespoke mix of salary and dividends to stay within lower tax brackets while enjoying the rewards of their portfolio. You can also use a Director’s Loan Account to recover your initial capital investment tax-free, as the company is simply repaying the debt it owes you. Beyond immediate income, share structuring offers a refined path for inheritance planning. By issuing different classes of shares, you can gift future capital growth to heirs while retaining control of the assets today. This proactive approach to inheritance tax ensures your legacy is protected from unnecessary erosion. For those seeking to refine their strategy, engaging in professional portfolio management can provide the oversight needed to maintain these complex financial structures.

Addressing the Objections: Higher Costs and ATED

While the corporate model offers significant advantages, it requires a clear-eyed assessment of the upfront and ongoing costs. It’s not a shortcut, but a professional framework that demands a higher entry price for long-term security. Specifically, the Stamp Duty Land Tax for corporate bodies now includes a 5% surcharge on top of standard residential rates. This initial outlay can feel substantial, yet it’s often the price of admission for a structure that protects your assets from the volatility of personal tax changes. Understanding the full tax implications of buying property in a company name uk means looking beyond the purchase date to the long-term administrative landscape.

Administrative overhead is another factor to weigh before incorporating. You’ll encounter accounting fees, annual filing requirements, and the need for absolute transparency with Companies House. Some investors worry about the “double taxation” trap, fearing they’ll pay tax twice on the same pound. In reality, with a disciplined approach to dividends and director loans, this is less a reality and more a myth that proper planning easily dispels. It’s about maintaining a rhythmic and orderly financial life where every penny is accounted for and every relief is claimed.

Navigating ATED in Prime London Markets

The Annual Tax on Enveloped Dwellings (ATED) is a specific consideration for those investing in London’s high-value postcodes. For the 2026/27 period, any property held in a company valued over £500,000 triggers an annual charge, starting at £4,600. In areas like Nine Elms and Westminster, staying beneath this threshold is rarely an option. However, genuine buy-to-let businesses can claim full relief from this charge. Ensuring you file the correct returns and maintain commercial letting status is where professional property management becomes indispensable. It provides the meticulous oversight needed to keep your portfolio compliant, your records accurate, and your mental tranquility intact.

The Reality of Corporate Mortgage Rates

Securing finance within an SPV typically carries higher interest rates than a standard personal mortgage. Lenders view corporate lending through a different risk lens, often requiring higher deposits and more rigorous stress tests. You aren’t just paying for the loan; you’re paying for the flexibility and scalability of a business structure. This higher interest is balanced by its status as a fully deductible expense, a benefit we’ve established as a cornerstone of corporate efficiency. Accessing elite mortgage consultations can help you navigate these bespoke products, ensuring you secure rates that reflect the prestige of your investment and the strength of your portfolio. It’s a calculated trade-off that prioritizes long-term growth over immediate, low-interest gratification.

Strategic Sourcing: Where to Buy in a Company Name

Selecting the right postcode is the final piece of the corporate investment puzzle. While the tax implications of buying property in a company name uk provide the financial framework, the asset itself determines the ultimate success of your legacy. New build property has emerged as the preferred asset class for corporate SPVs, offering a combination of energy efficiency, modern aesthetics, and lower maintenance liabilities. These properties typically carry ten year warranties and high EPC ratings, which simplify the facilities management process and ensure your business remains compliant with evolving environmental regulations. By focusing on premium developments, you align your corporate structure with assets that attract high-caliber tenants and offer steady capital growth.

High-Yield Opportunities in Canary Wharf and Nine Elms

Districts like Canary Wharf and Nine Elms are particularly suited for corporate ownership due to their institutional-grade infrastructure and strong rental demand. These hubs are populated by professional tenants who value high-end finishes and lifestyle amenities, mirroring the prestige of your own investment vehicle. When you buy in these high-growth areas, you’re investing in a district’s future as much as a single unit. For a deeper look at specific district performance, our guide to real estate in england london provides the data needed to make an informed decision. The tax implications of buying property in a company name uk become even more favorable when rental yields are high enough to cover corporate interest payments while leaving a surplus for reinvestment.

The Off-Plan Advantage for Companies

Building a portfolio through off-plan acquisitions allows a company to lock in current market prices for future assets. This strategy is ideal for managing cash flow, as it requires a smaller initial deposit while the property is under construction, allowing your corporate capital to remain fluid. It provides a rhythmic approach to growth, where new assets are added to the balance sheet in a predictable sequence. To understand how to navigate these opportunities safely, explore our resources on off-plan property investment for risk mitigation strategies. This forward-thinking approach ensures your company is always positioned ahead of the market curve.

If you’re ready to identify your next high-value asset, our team offers bespoke property sourcing tailored to your corporate goals.

MaddisonV: Your Partner in Corporate Property Excellence

Understanding the tax implications of buying property in a company name uk is only the first chapter of a successful investment story. The second chapter is execution. MaddisonV serves as your premium partner, bridging the gap between sophisticated financial planning and the physical acquisition of high-tier London assets. We recognize that for our clients, property is more than just a line on a balance sheet; it’s a legacy that requires a meticulous and detail-oriented approach. Our role is to handle the complex operational details, from initial sourcing to ongoing oversight, so you can enjoy the rewards of your portfolio with complete mental tranquility. We provide a bridge between clinical management and a genuine appreciation for superior user experiences.

Our commitment to excellence means we don’t just find properties; we curate opportunities. By connecting our clients with elite tax advisors and mortgage specialists, we ensure that every corporate acquisition is built on a foundation of financial security and professional order. Whether you’re targeting a sleek new development in Canary Wharf or a prestigious residence in Westminster, our team ensures the process is fluid, transparent, and entirely aligned with your long-term scalability goals. We take pride in the visual and functional standards of the portfolios we manage, ensuring nothing is left to chance in the pursuit of your investment legacy.

The MaddisonV Sourcing Framework

We’ve developed a sourcing framework that prioritizes assets specifically suited for corporate SPVs. This involves a level of due diligence that goes far beyond the surface, examining everything from EPC ratings to the long-term growth potential of specific London districts. As dedicated property sourcing agents London, we operate on a success-based fee model that ensures our interests are perfectly aligned with yours. We focus on identifying off-plan opportunities and new build properties that offer the highest standards of energy efficiency and modern aesthetics, reducing your company’s future maintenance liabilities and enhancing asset protection.

Effortless Management for Discerning Owners

The true value of corporate ownership is the ability to scale without increasing your personal administrative burden. Our facilities management and portfolio oversight services are designed to preserve the passive nature of your investment. We ensure that your corporate tenants receive a five-star experience, which in turn protects your rental yields and maintains the prestige of your brand. From handling daily operational tasks to ensuring ATED compliance and meticulous record-keeping, we provide a polished, all-encompassing solution. This allows you to maintain a professional distance while your portfolio grows with steady, rhythmic precision. If you’re ready to elevate your strategy, explore our exclusive London investment opportunities and discover a partnership built on integrity and high-tier standards.

Building Your Multi-Generational Property Legacy

Transitioning to a corporate structure is more than a tax strategy; it’s a commitment to professional excellence and long-term security. By embracing the full deductibility of mortgage interest and the efficiency of corporate tax rates, you position your portfolio for effortless, scalable growth. Navigating the tax implications of buying property in a company name uk ensures that your acquisitions in Canary Wharf or Nine Elms remain protected, profitable, and ready for future generations. It’s about creating a structure that handles the complex operational details so you don’t have to. Execution is everything.

Our specialists focus on high-tier new builds, providing comprehensive sourcing and facilities management that preserve the passive nature of your partnership. We connect you with an elite network of mortgage and tax advisors to ensure every detail is handled with meticulous care. Your journey toward a sophisticated property legacy starts with a single, well-considered decision. Take the next step toward financial order and mental tranquility today.

Secure your London investment future with a bespoke consultation

Frequently Asked Questions

Is it better to buy property in a company name or personally in 2026?

Corporate ownership is often the superior choice for higher-rate taxpayers in 2026. This is primarily because companies can fully deduct mortgage interest as a business expense, whereas individuals are restricted to a 20% tax credit. For professional investors, the corporate structure offers better scalability, significant tax efficiencies, and a layer of asset protection that personal holding cannot match. Understanding the tax implications of buying property in a company name uk is essential for those building a multi-generational legacy.

How much is Corporation Tax for a UK property company?

The main rate of Corporation Tax for the 2026/27 financial year is 25% for companies with profits exceeding £250,000. For smaller companies with profits up to £50,000, a small profits rate of 19% applies. Companies with profits between these two figures may benefit from marginal relief. This structure provides a predictable and manageable tax environment as your London portfolio grows in value, complexity, and prestige.

Can I move my existing properties into a limited company?

You can transfer existing properties into a limited company, but it’s treated as a sale at current market value. This process often triggers Capital Gains Tax for you personally and Stamp Duty Land Tax for the company. Because of these substantial upfront costs, many sophisticated investors prefer to use a company for new acquisitions in districts like Canary Wharf or Battersea rather than moving established personal assets into a corporate envelope.

What is the 15% Stamp Duty rate for companies?

While the question references 15%, a 17% flat rate of Stamp Duty Land Tax actually applies to companies purchasing residential properties valued over £500,000. However, most genuine property rental businesses are eligible for relief from this higher rate. Instead, they pay the standard residential rates plus the 5% corporate surcharge. This ensures that professional investment vehicles aren’t unfairly penalized for high-value acquisitions in Westminster or Nine Elms, provided they’re let on a commercial basis.

Do I have to pay Capital Gains Tax when a company sells a property?

Companies don’t pay Capital Gains Tax; instead, any profit from a sale is subject to Corporation Tax at the prevailing rate. This is a vital part of the tax implications of buying property in a company name uk, as it allows for a more fluid treatment of gains within the business structure. While individuals have a small £3,000 annual exempt amount, companies benefit from a more institutional framework for reinvesting capital into new developments.

What is an SPV in the context of UK property investment?

A Special Purpose Vehicle, or SPV, is a limited company established exclusively for the purpose of buying, selling, and letting property. Lenders prefer this “clean” financial structure because it separates property assets from other trading risks, which often results in more streamlined mortgage applications. Using an SPV is the standard approach for sophisticated investors who value financial security, operational clarity, and long-term portfolio scalability.

Are mortgage rates higher for limited companies than for individuals?

Mortgage rates for limited companies are generally higher than those offered to individual borrowers due to the increased complexity of corporate underwriting. However, the ability to fully deduct these interest payments as a business expense often offsets the higher headline rate. For many, the trade-off is worthwhile for the enhanced tax efficiency and the ability to grow a portfolio without the personal income tax constraints imposed by Section 24.

How does ATED affect my London property investment?

The Annual Tax on Enveloped Dwellings (ATED) applies to companies holding UK residential property valued at more than £500,000. While the annual charges can be significant, starting at £4,600 for the 2026/27 period, full relief is available for properties let to third parties on a commercial basis. Even when claiming relief, you must file an annual return by 30 April to maintain compliance, ensure mental tranquility, and avoid unnecessary penalties.

Sign Up Now

Want to read more great articles and blogs subscribe to our newsletter